equityCurve

Description

equityCurve( plots the equity

curves of each strategy that you create using backtester)backtestStrategy. After creating

the backtesting engine using backtestEngine and running the

backtest with runBacktest, use

equityCurve to plot the strategies and compare their

performance.

h = equityCurve(ax,backtester)h.

Examples

Generate Equity Curve for Backtest

The MATLAB® backtesting engine runs backtests of portfolio investment strategies over time series of asset price data. After creating a set of backtest strategies using backtestStrategy and the backtesting engine using backtestEngine, the runBacktest function executes the backtest. After using the runBacktest function to test investment strategies, you can run the equityCurve function to plot the equity curves of strategies.

Load Data

Load one year of stock price data. For readability, this example uses only a subset of the DJIA stocks.

% Read a table of daily adjusted close prices for 2006 DJIA stocks T = readtable('dowPortfolio.xlsx'); % Prune the table to hold only the dates and selected stocks timeColumn = "Dates"; assetSymbols = ["BA", "CAT", "DIS", "GE", "IBM", "MCD", "MSFT"]; T = T(:,[timeColumn assetSymbols]); % Convert to timetable pricesTT = table2timetable(T,'RowTimes','Dates'); % View the final asset price timetable head(pricesTT)

Dates BA CAT DIS GE IBM MCD MSFT

___________ _____ _____ _____ _____ _____ _____ _____

03-Jan-2006 68.63 55.86 24.18 33.6 80.13 32.72 26.19

04-Jan-2006 69.34 57.29 23.77 33.56 80.03 33.01 26.32

05-Jan-2006 68.53 57.29 24.19 33.47 80.56 33.05 26.34

06-Jan-2006 67.57 58.43 24.52 33.7 82.96 33.25 26.26

09-Jan-2006 67.01 59.49 24.78 33.61 81.76 33.88 26.21

10-Jan-2006 67.33 59.25 25.09 33.43 82.1 33.91 26.35

11-Jan-2006 68.3 59.28 25.33 33.66 82.19 34.5 26.63

12-Jan-2006 67.9 60.13 25.41 33.25 81.61 33.96 26.48

Create Strategy

Test an equal-weighted investment strategy. This strategy invests an equal portion of the available capital into each asset. This example does not describe how to create backtesting strategies. For more information on creating backtesting strategies, see backtestStrategy.

Set 'RebalanceFrequency' to rebalance the portfolio every 60 days. This example does not use a lookback window to rebalance.

% Create the strategy numAssets = size(pricesTT,2); equalWeightsVector = ones(1,numAssets) / numAssets; equalWeightsRebalanceFcn = @(~,~) equalWeightsVector; ewStrategy = backtestStrategy("EqualWeighted",equalWeightsRebalanceFcn, ... 'RebalanceFrequency',60, ... 'LookbackWindow',0, ... 'TransactionCosts',0.005, ... 'InitialWeights',equalWeightsVector)

ewStrategy =

backtestStrategy with properties:

Name: "EqualWeighted"

RebalanceFcn: @(~,~)equalWeightsVector

RebalanceFrequency: 60

TransactionCosts: 0.0050

LookbackWindow: 0

InitialWeights: [0.1429 0.1429 0.1429 0.1429 0.1429 0.1429 0.1429]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0x0 struct]

EngineDataList: [0x0 string]

Run Backtest

Create a backtesting engine and run a backtest over a year of stock data. For more information on creating backtest engines, see backtestEngine.

% Create the backtesting engine. The backtesting engine properties that hold the % results are initialized to empty. backtester = backtestEngine(ewStrategy)

backtester =

backtestEngine with properties:

Strategies: [1x1 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: []

Returns: []

Positions: []

Turnover: []

BuyCost: []

SellCost: []

TransactionCosts: []

Fees: []

% Run the backtest. The empty properties are now populated with % timetables of detailed backtest results. backtester = runBacktest(backtester,pricesTT)

backtester =

backtestEngine with properties:

Strategies: [1x1 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: 7

Returns: [250x1 timetable]

Positions: [1x1 struct]

Turnover: [250x1 timetable]

BuyCost: [250x1 timetable]

SellCost: [250x1 timetable]

TransactionCosts: [1x1 struct]

Fees: [1x1 struct]

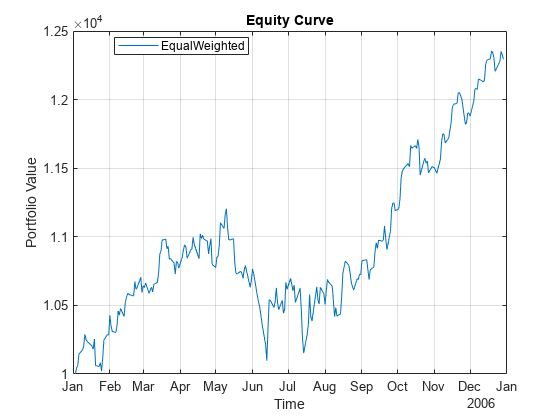

Generate Equity Curve

Use the equityCurve to plot the equity curve for the equal-weight strategy.

equityCurve(backtester)

Input Arguments

Output Arguments

Version History

Introduced in R2021a

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)