Portfolio Optimization Using Social Performance Measure

Use a Portfolio object to minimize the variance, maximize return, and maximize the average percentage of women on a company's board. The same workflow can be applied with other Environmental, Social and Governance (ESG) criteria, such as an ESG score, a climate, or a temperature score.

The goal of this example is to find portfolios that are effcient in the sense that they minimize the variance, maximize return, and maximize the average percentage of women on the board of directors. To find the average percentage of women on a company's board (WoB) for a given portfolio, this example uses a weighted sum of the percentages of WoB for each individual asset, where the weights are given by the amount invested in each asset for the portfolio. By defining the average percentage of WoB this way, the WoB function is linear with respect to the weights.

Load Portfolio Data

load CAPMuniverse % Assume that the percentage of women on the board of directors per % company are as follows WoB = [0.2857; 0.5; 0.3; 0.2857; 0.3077; 0.2727; ... 0.4167; 0.2143; 0.3; 0.4167; 0.3077]; table(WoB,'VariableNames',{'WoB'},'RowNames',Assets(1:11))

ans=11×1 table

WoB

______

AAPL 0.2857

AMZN 0.5

CSCO 0.3

DELL 0.2857

EBAY 0.3077

GOOG 0.2727

HPQ 0.4167

IBM 0.2143

INTC 0.3

MSFT 0.4167

ORCL 0.3077

Create Portfolio Object

Create a standard Portfolio object and incorporate the list of assets and estimate the moments of the assets' returns from the data. Use setDefaultConstraints to set the default mean-variance portfolio constraints. These constraints require fully invested, long-only portfolios where the nonnegative weights must sum to 1.

% Create portfolio with default constraints p = Portfolio('AssetList',Assets(1:11)); p = estimateAssetMoments(p, Data(:,1:11)); p = setDefaultConstraints(p);

Set Group Constraints

Use getGroups to include group contraints. The first group constraint ensures that the weights invested in mixed retail (Amazon and eBay) are at least 15%. The second group constraint ensures that the weights invested in computer companies (Apple, Dell and HP) are between 25% and 50%.

% Group constraints

G = [0 1 0 0 1 0 0 0 0 0 0;

1 0 0 1 0 0 1 0 0 0 0];

LowG = [0.15; 0.25];

UpG = [Inf; 0.5];

p = setGroups(p, G, LowG, UpG);Find the minimum and maximum percentage of WoB that a portfolio can attain given these extra group constraints. This is done using the estimateCustomObjectivePortfolio function with the average percentage of women on a company's board as the objective function.

% Set average WoB as the objective

objFun = @(x) WoB'*x;Find the portfolio with the minimum average percentage of WoB with the group constraints using estimateCustomObjectivePortfolio with the function handle objFun.

% Minimum percetage of women on the board

wgt_minWoB = estimateCustomObjectivePortfolio(p,objFun);

minWoB = objFun(wgt_minWoB)minWoB = 0.2462

Find the portfolio with the maximum average percentage of WoB with the group constraints using estimateCustomObjectivePortfolio with the name-value argument ObjectiveSense set to maximize.

% Maximum percentage of women on the board wgt_maxWoB = estimateCustomObjectivePortfolio(p,objFun,... ObjectiveSense="maximize"); maxWoB = objFun(wgt_maxWoB)

maxWoB = 0.4792

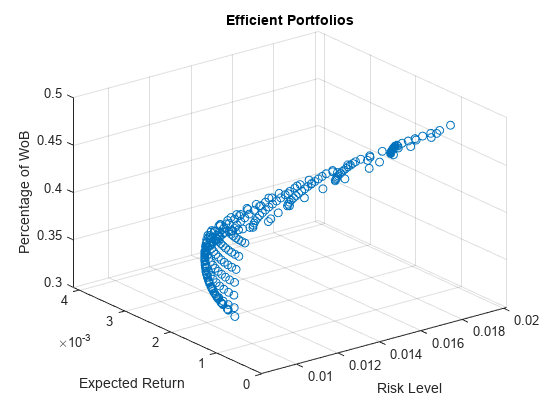

Compute and Plot the Efficient Surface

Define a grid of WoB percentages such that minWoB targetWoB(1) targetWoB(N) maxWoB.

N = 20; % Size of grid

targetWoB = linspace(minWoB,maxWoB,N);Use setInequality to set the percentage of WoB as a constraint. The coefficients of the linear constraint should be the WoB percentages associated to each asset, and the right-hand side should be the target portfolio WoB. The convention of the inequality is . Since the goal is to maximize portfolio WoB, then the target WoB should be a lower bound for the portfolio WoB. Therefore, the signs of the coefficients and the right-hand side of the added inequality should be flipped.

Ain = -WoB';

bin = -minWoB; % Start with the smallest WoB

p = setInequality(p,Ain,bin);For each target WoB, targetWoB(i), find the efficient mean-variance frontier using estimateFrontier. At each iteration, the right-hand side of the WoB portfolio constraint should be changed to ensure that the returned portfolios achieve at least the target WoB. This method returns the weights of the portfolios on the mean-variance efficient frontier that have a WoB of at least targetWoB(i). Using the weights obtained for each target WoB, compute the portfolios' expected return, risk, and percentage of WoB.

% Get efficient surface values prsk = cell(N,1); pret = cell(N,1); pWoB = cell(N,1); for i = 1:N p.bInequality = -targetWoB(i); pwgt = estimateFrontier(p,N); [prsk{i},pret{i}] = estimatePortMoments(p,pwgt); pWoB{i} = pwgt'*WoB; end

Plot the efficient portfolios.

% Plot efficient surface scatter3(cell2mat(prsk),cell2mat(pret),cell2mat(pWoB)) title('Efficient Portfolios') xlabel('Risk Level') ylabel('Expected Return') zlabel('Percentage of WoB')

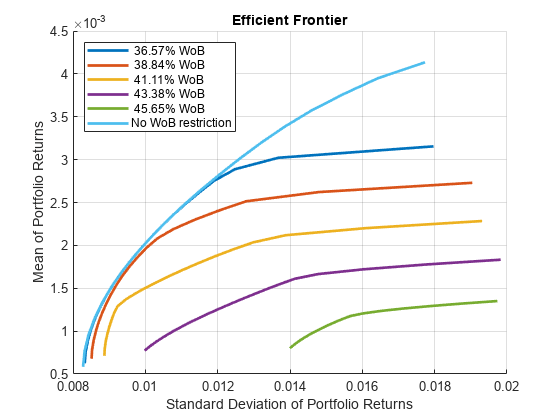

To visualize the tradeoff between a portfolio's average percentage of WoB and the traditional mean-variance efficient frontier, a set of contour plots are computed for some target WoB percentages using the plotContours function in Local Functions.

nC = 5; % Number of contour plots minContour = max(pWoB{1}); % WoB values lower than this return % overlapped contours. % Plot contours plotContours(p,minContour,maxWoB,nC,N)

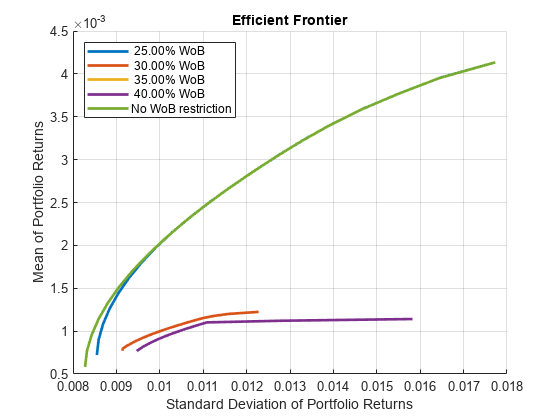

Exclusion Examples

Instead of requiring a specific level for the portfolio's average percentage of WoB, the goal is to find the traditional mean-variance efficient frontiers while excluding assets that have a percentage of WoB lower than a given threshold. You can plot the exclusion using the plotExclusionExample function in Local Functions.

% Remove the average percetage of WoB constraint p.AInequality = []; p.bInequality = []; % Set of thresholds for excluding assets thresholdWoB = 0.25:0.05:0.40; % Plot exclusion example plotExclusionExample(p,WoB,thresholdWoB,N)

The differences between this approach and the one presented in the previous section are quite evident. Requiring all the assets to have a WoB percentage of at least 35% gives an efficient frontier that can achieve a return of at most around . On the other hand, requiring only that the portfolio's average percentage of WoB is 36.57% gives the possibility to reach a return of around , almost 2.5 times the return obtained when excluding assets. To better show the differences between these two approaches, compute the maximum return achieved for a given standard deviation for the two ways of including the percentage of WoB requirements to the portfolio.

Approach 1

In the first approach, exclude all assets with a WoB percentage lower than 33% and find the portfolio of maximum return that has a standard deviation of at most 0.012.

% Select assets to exclude ub = zeros(p.NumAssets,1); ub(WoB >= 0.33) = 1; p.UpperBound = ub; % Estimate the return for a risk level of 0.012 pwgt_exclude = estimateFrontierByRisk(p,0.012); ret_exclude = estimatePortReturn(p,pwgt_exclude)

ret_exclude = 0.0011

% Return constraints to the original portfolio

p.UpperBound = [];Approach 2

For the second approach, ensure that the average WoB percentage is of at least 33% and find the portfolio of maximum return that has a standard deviation of at most 0.012.

% Include WoB constraint into the portfolio p = addInequality(p,-WoB',-0.33); % Estimate the return for a risk level of 0.012 pwgt_avgWoB = estimateFrontierByRisk(p,0.012); ret_avgWoB = estimatePortReturn(p,pwgt_avgWoB)

ret_avgWoB = 0.0028

% Return constraints to the original portfolio

p.AInequality = []; p.bInequality = [];Compute the increase in return between these two approaches.

ret_increase = (ret_avgWoB-ret_exclude)/ret_exclude

ret_increase = 1.5202

This ret_increase value shows that the return from the approach that only bounds the portfolio's average WoB percentage instead of excluding certain assets has a return 152% higher (for the same risk level). Hence, when tackling problems with more than two objectives, excluding assets that do not meet a certain criteria might not be the best option. Instead, a weighted sum of the criteria of interest might show better results.

Local Functions

function [] = plotContours(p,minWoB,maxWoB,nContour,nPort) % Set of WoB levels for contour plot contourWoB = linspace(minWoB,maxWoB,nContour+1); % Compute and plot efficient frontier for each value in contourWoB figure; hold on labels = strings(nContour+1,1); for i = 1:nContour p.bInequality = -contourWoB(i); plotFrontier(p,nPort); labels(i) = sprintf("%6.2f%% WoB",contourWoB(i)*100); end % Plot the "original" mean-variance frontier, i.e., the frontier % without WoB requierements p.AInequality = []; p.bInequality = []; plotFrontier(p,nPort); labels(i+1) = "No WoB restriction"; legend(labels,'Location','northwest') hold off end function [] = plotExclusionExample(p,WoB,thresholdWoB, ... nPort) % Compute and plot efficient frontier excluding assets that are below % the WoB threshold nT = length(thresholdWoB); figure; hold on labels = strings(nT+1,1); for i=1:nT ub = zeros(p.NumAssets,1); % Only select assets above WoB threshold ub(WoB >= thresholdWoB(i)) = 1; p.UpperBound = ub; plotFrontier(p,nPort); labels(i) = sprintf("%6.2f%% WoB",thresholdWoB(i)*100); end % Plot the "original" mean-variance frontier, i.e., the frontier % without the WoB threshold p.UpperBound = []; plotFrontier(p,nPort); labels(i+1) = "No WoB restriction"; legend(labels,'Location','northwest') hold off end

See Also

Portfolio | setBounds | addGroups | setAssetMoments | estimateAssetMoments | estimateBounds | plotFrontier | estimateFrontierLimits | estimateFrontierByRisk | estimatePortRisk

Related Examples

- Creating the Portfolio Object

- Working with Portfolio Constraints Using Defaults

- Validate the Portfolio Problem for Portfolio Object

- Estimate Efficient Portfolios for Entire Efficient Frontier for Portfolio Object

- Estimate Efficient Frontiers for Portfolio Object

- Postprocessing Results to Set Up Tradable Portfolios

- Portfolio Optimization with Semicontinuous and Cardinality Constraints

- Black-Litterman Portfolio Optimization Using Financial Toolbox

- Portfolio Optimization Against a Benchmark

- Portfolio Optimization Examples Using Financial Toolbox

- Diversify Portfolios Using Custom Objective

More About

External Websites

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)