Lifetime Models for Probability of Default

Develop and validate Lifetime models for probability of default (PD) based on a lifetime analysis conditional on macroeconomic scenarios. Calculate the estimated loss reserves using Expected Credit Loss (ECL) calculator.

Functions

Objects

Logistic | Create Logistic model object for lifetime probability of

default (Since R2020b) |

Probit | Create Probit model object for lifetime probability of

default (Since R2020b) |

Cox | Create Cox model object for lifetime probability of

default (Since R2021b) |

customLifetimePDModel | Create customLifetimePDModel object for lifetime probability

of default (Since R2022b) |

Topics

- Overview of Lifetime Probability of Default Models

Estimate loss reserves based on a lifetime analysis conditional on macroeconomic scenarios.

- Basic Lifetime PD Model Validation

This example shows how to perform basic model validation on a lifetime probability of default (PD) model by viewing the fitted model, estimated coefficients, and p-values.

- Compare Logistic Model for Lifetime PD to Champion Model

This example shows how to compare a new

Logisticmodel for lifetime PD against a "champion" model. - Compare Lifetime PD Models Using Cross-Validation

This example shows how to compare three lifetime PD models using cross-validation.

- Expected Credit Loss Computation

This example shows how to perform expected credit loss (ECL) computations with

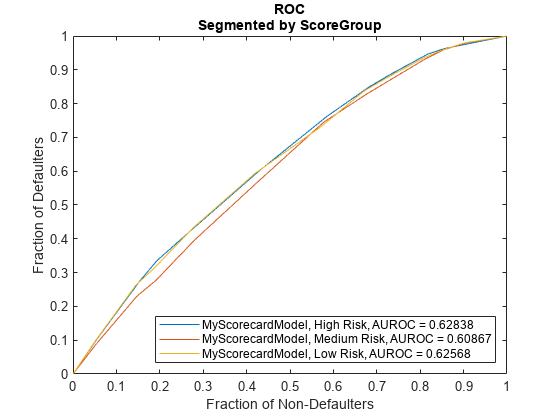

portfolioECLusing simulated loan data, macro scenario data, and an existing lifetime probability of default (PD) model. - Compare Model Discrimination and Model Calibration to Validate of Probability of Default

This example shows some differences between discrimination and calibration metrics for the validation of probability of default (PD) models.

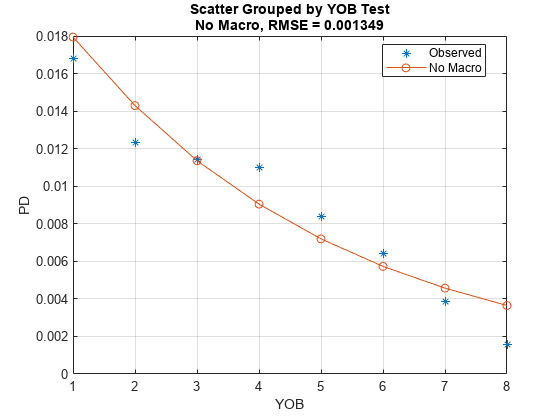

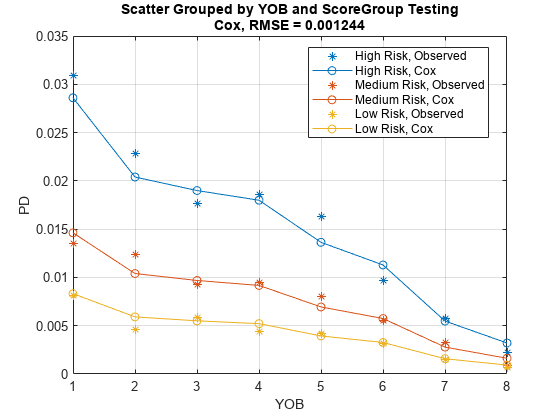

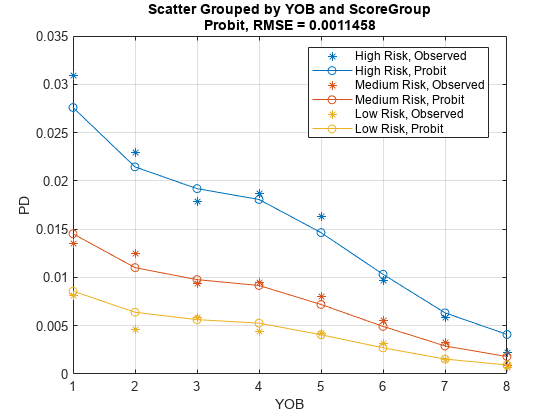

- Modeling Probabilities of Default with Cox Proportional Hazards

This example shows how to work with consumer (retail) credit panel data to visualize observed probabilities of default (PDs) at different levels.

- Interpret and Stress-Test Deep Learning Networks for Probability of Default

Train a credit risk for probability of default (PD) prediction using a deep neural network.

- Create Custom Lifetime PD Model for Credit Scorecard Model with Function Handle

This example shows how to use

customLifetimePDModelto create a lifetime model for the probability of default. - Create Custom Lifetime PD Model for Decision Tree Model with Function Handle

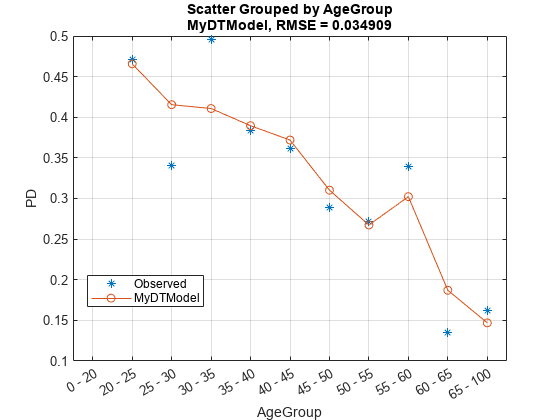

This example shows how to fit a decision tree model for credit scoring and then use the

customLifetimePDModelobject to create a lifetime model for probability of default. - Incorporate Macroeconomic Scenario Projections in Loan Portfolio ECL Calculations

This example shows how to generate macroeconomic scenarios and perform expected credit loss (ECL) calculations for a portfolio of loans.

- Create Weighted Lifetime PD Model

This example shows how to use

fitLifetimePDModelto create a PD model using weighted credit and macroeconomic data.

Featured Examples

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)