Pricing Mortgage Backed Securities Using Black-Derman-Toy Model

This example illustrates how the Financial Toolbox™ and Financial Instruments Toolbox™ are used to price a level mortgage backed security using the BDT model.

Load the BDT Tree Stored in Data File

load mbsexample.matObserve Interest-Rate Tree

Visualize the interest rate evolution along the tree by looking at the output structure BDTTree. BDTTree returns an inverse discount tree, which you can convert into an interest-rate tree with the cvtree function.

BDTTreeR = cvtree(BDTTree);

Look at the upper branch and lower branch paths of the tree:

OldFormat = get(0, 'format'); format short %Rate at root node: RateRoot = treepath(BDTTreeR.RateTree, 0)

RateRoot = 0.0399

%Rates along upper branch:

RatePathUp = treepath(BDTTreeR.RateTree, [1 1 1 1 1]) RatePathUp = 6×1

0.0399

0.0397

0.0391

0.0383

0.0373

0.0360

%Rates along lower branch:

RatePathDown = treepath(BDTTreeR.RateTree, [2 2 2 2 2])RatePathDown = 6×1

0.0399

0.0470

0.0550

0.0638

0.0734

0.0841

Compute the Price Tree for Non-Prepayable Mortgage

Assume that you have a three year $10000 level prepayable loan, with a mortgage interest rate of 4.64% semi-annually compounded.

MortgageAmount = 10000; CouponRate = 0.0464; Period = 2; Settle='01-Jan-2007'; Maturity='01-Jan-2010'; Compounding = BDTTree.TimeSpec.Compounding; format bank

Use the function amortize in the Financial Toolbox™ to calculate the mortgage payment of the loan (MP), the interest and principal components, and the outstanding principal balance.

NumPeriods = date2time(Settle,Maturity, Compounding)';

[Principal, InterestPayment, OutstandingBalance, MP] = amortize(CouponRate/Period, NumPeriods, MortgageAmount);

% Display Principal, Interest and Outstanding balances

PrincipalAmount = Principal'PrincipalAmount = 6×1

1572.59

1609.07

1646.40

1684.60

1723.68

1763.67

InterestPaymentAmount = InterestPayment'

InterestPaymentAmount = 6×1

232.00

195.52

158.19

119.99

80.91

40.92

OutstandingBalanceAmount = OutstandingBalance'

OutstandingBalanceAmount = 6×1

8427.41

6818.34

5171.94

3487.35

1763.67

0.00

CFlowAmounts = MP*ones(1,NumPeriods); % The CFlowDates are the same as the tree level dates CFlowDates= {'01-Jul-2007' ,'01-Jan-2008' ,'01-Jul-2008' , '01-Jan-2009' , '01-Jul-2009' , '01-Jan-2010'} ; % Calculate the price of the non-prepayable mortgage [PriceNonPrepayableMortgage, PriceTreeNonPrepayableMortgage] = cfbybdt(BDTTree, CFlowAmounts, CFlowDates, Settle); for iLevel = 2:length(PriceTreeNonPrepayableMortgage.PTree) PriceTreeNonPrepayableMortgage.PTree{iLevel}(:,:)= PriceTreeNonPrepayableMortgage.PTree{iLevel}(:,:) - MP; end % Look at the price of the mortgage today tObs = 0 PriceNonPrepayableMortgage

PriceNonPrepayableMortgage =

10017.47

% The value of the non-prepayable mortgage is $10017.47. This value exceeds % the $10000 amount borrowed since the homeowner received not only $10000, but % also a prepayment option. % Look at the value of the mortgage on the last date, right after the last % mortgage payment, is zero: PriceTreeNonPrepayableMortgage.PTree{end}

ans = 1×6

0 0 0 0 0 0

% Visualize the price tree for the non-prepayable mortgage.

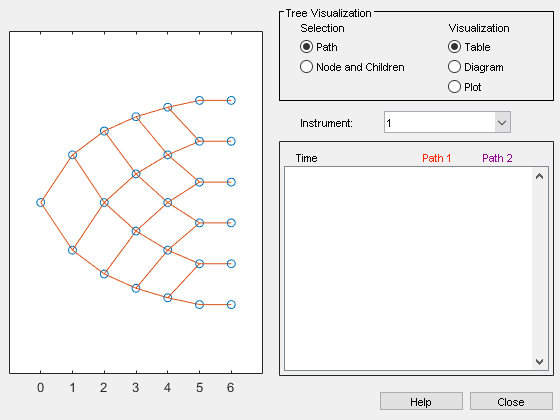

treeviewer(PriceTreeNonPrepayableMortgage)

Compute Price Tree of Prepayment Option

% The Prepayment option is like a call option on a bond. % % The exercise price or strike will be equal to the outstanding principal amount % which has been calculated using the function amortize. OptSpec = 'call'; Strike = [MortgageAmount OutstandingBalance]; ExerciseDates =[Settle CFlowDates]; AmericanOpt = 0; Maturity = CFlowDates(end); % Compute the price of the prepayment option: [PricePrepaymentOption, PriceTreePrepaymentOption] = prepaymentbybdt(BDTTree, OptSpec, Strike, ExerciseDates, AmericanOpt, ... 0, Settle, Maturity,[], [], [], ... [], [], [], [], 0, [], CFlowAmounts); % Look at the price of the prepayment option today (tObs = 0) PricePrepaymentOption

PricePrepaymentOption =

17.47

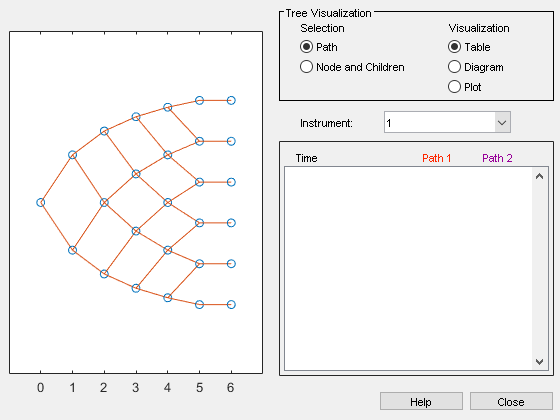

% The value of the prepayment option is $17.47 as expected. % Visualize the price tree for the prepayment option treeviewer(PriceTreePrepaymentOption)

Calculate Price Tree of Prepayable Mortgage

% Compute the price of the prepayable mortgage. PricePrepayableMortgage = PriceNonPrepayableMortgage - PricePrepaymentOption; PriceTreePrepayableMortgage = PriceTreeNonPrepayableMortgage; for iLevel = 1:length(PriceTreeNonPrepayableMortgage.PTree) PriceTreePrepayableMortgage.PTree{iLevel}(:,:) = PriceTreeNonPrepayableMortgage.PTree{iLevel}(:,:) - ... PriceTreePrepaymentOption.PTree{iLevel}(:,:); end % Look at the price of the prepayable mortgage today (tObs = 0) PricePrepayableMortgage

PricePrepayableMortgage =

10000.00

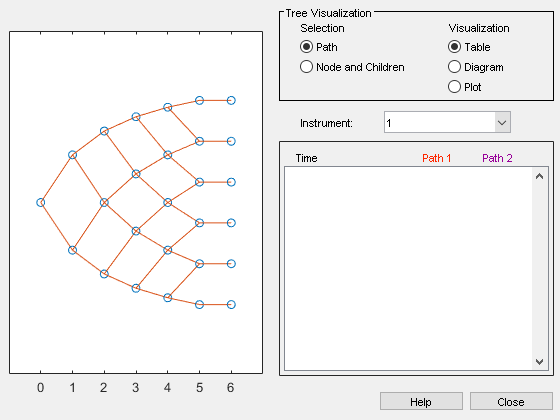

% The value of the prepayable mortgage is $10000 as expected. % Visualize the price and price tree for the prepayable mortgage treeviewer(PriceTreePrepayableMortgage)

set(0, 'format', OldFormat);See Also

mbscfamounts | mbsconvp | mbsconvy | mbsdurp | mbsdury | mbsnoprepay | mbspassthrough | mbsprice | mbswal | mbsyield | mbsprice2speed | mbsyield2speed | psaspeed2default | psaspeed2rate | mbsoas2price | mbsoas2yield | mbsprice2oas | mbsyield2oas

Related Examples

- Prepayment Modeling with a Two Factor Hull White Model and a LIBOR Market Model

- Using Collateralized Mortgage Obligations (CMOs)

More About

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)