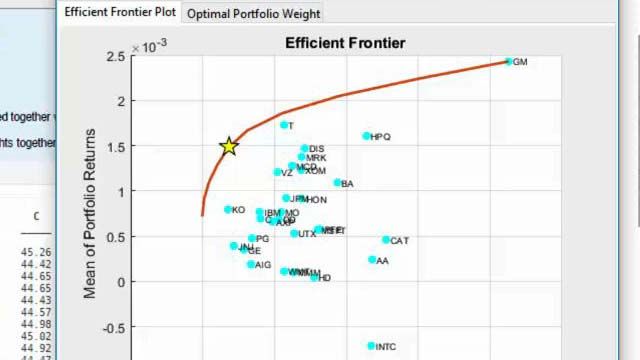

Portfolio optimization is a mathematical approach to making investment decisions across a collection of financial instruments or assets. The goal of portfolio optimization is to find the mix of investments that achieve a desired risk versus return tradeoff. The conventional method for portfolio optimization is mean-variance portfolio optimization, which is based on the assumption that returns are normally distributed.

On the other hand, conditional value-at-risk (CVaR) is the extended risk measure of value-at-risk that quantifies the average loss over a specified time period of scenarios beyond the confidence level. For example, a one-day 99% CVaR of $12 million means the expected loss of the worst 1% scenarios over a one-day period is $12 million. Moreover, CVaR is also known as expected shortfall.

With CVaR portfolio optmization, you do not need to assume normally distributed returns. In this example, you will learn:

- How to use copula to generate correlated asset scenarios that try to mimic the pattern of historical returns

- How to apply CVaR portfolio optimization based on simulated asset scenarios

- How to compare the efficient frontiers between CVaR portfolio optimization and mean-variance portfolio optimization