Risk and Asset Allocation

These routines support the book "Risk and Asset Allocation" Springer Finance, by A. Meucci, see http://www.symmys.com

The routines include many new features:

- more uni-, multi- and matrix-variate distributions

- more copulas

- more graphical representations

- more analyses in terms of the location-dispersion ellipsoid.

- best replication / best factor selection

- FFT-based projection of a distribution to the investment horizon

- caveats about delta/gamma pricing

- step-by-step evaluation of a generic estimator

- non-parametric estimators

- multivariate elliptical maximum-likelihood estimators

- shrinkage estimators: Stein and Ledoit-Wolf, Bayesian classical equivalent

- robust estimators: Hubert M, high-breakdown minimum volume ellipsoid

- missing-data techniques: EM algorithm, uneven-series conditional estimation

- stochastic dominance

- extreme value theory for VaR

- Cornish-Fisher approximation for VaR

- kernel-based contribution to VaR and expected shortfall from different risk-factors

- mean-variance analysis and pitfalls (different horizons, compounded vs. linear returns, etc...)

- Bayesian estimation (multivariate analytical, Monte Carlo Markov Chains, priors for correlation matrices)

- estimation risk evaluation: opportunity cost of estimation-based allocations

- Black Litterman allocation

- robust optimization (calls SeDuMi to perform cone programming)

- robust Bayesian allocation

- more...

In addition to these MATLAB routines, at www.symmys.com the reader can find other freely downloadable complementary materials:

- the "Technical Appendices", a booklet with the proofs of the results presented in the books and used in the routines

- the "Slides", a set of presentations that walk the reader through the whole book

- the "Errata", a few typos in the first two reprints of the book

- the "Sample", an excerpt of the book.

Any feedback on the above materials is highly appreciated: please refer to www.symmys.com to contact the author.

Cite As

Attilio Meucci (2023). Risk and Asset Allocation (/matlabcentral/fileexchange/9061-risk-and-asset-allocation), MATLAB Central File Exchange. Retrieved .

MATLAB Release Compatibility

Platform Compatibility

Windows macOS LinuxCategories

- Computational Finance > Financial Toolbox > Portfolio Optimization and Asset Allocation >

- Computational Finance > Risk Management Toolbox >

- Computational Finance > Econometrics Toolbox > Conditional Variance Models >

Tags

Community Treasure Hunt

Find the treasures in MATLAB Central and discover how the community can help you!

Start Hunting!Discover Live Editor

Create scripts with code, output, and formatted text in a single executable document.

AMeucciRiskandAssetAllocationRoutines/Ch1_UniVariateDistributions/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/A_Distributions/Cdf/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/A_Distributions/Pdf/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/A_Distributions/Simulations/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/A_Distributions/Simulations/Elliptical/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/B_Copulas/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/B_Copulas/A_pdf/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/B_Copulas/B_cdf/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/B_Copulas/C_Simulations/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/B_Copulas/D_DependenceStatistics/

AMeucciRiskandAssetAllocationRoutines/Ch2_MultiVariateDistributions/C_LocationDispersion/

AMeucciRiskandAssetAllocationRoutines/Ch3_ModellingMarket/A_InvarianceQuest/

AMeucciRiskandAssetAllocationRoutines/Ch3_ModellingMarket/B_HorizonProjection/

AMeucciRiskandAssetAllocationRoutines/Ch3_ModellingMarket/C_DimensionReduction/

AMeucciRiskandAssetAllocationRoutines/Ch3_ModellingMarket/D_Pricing/

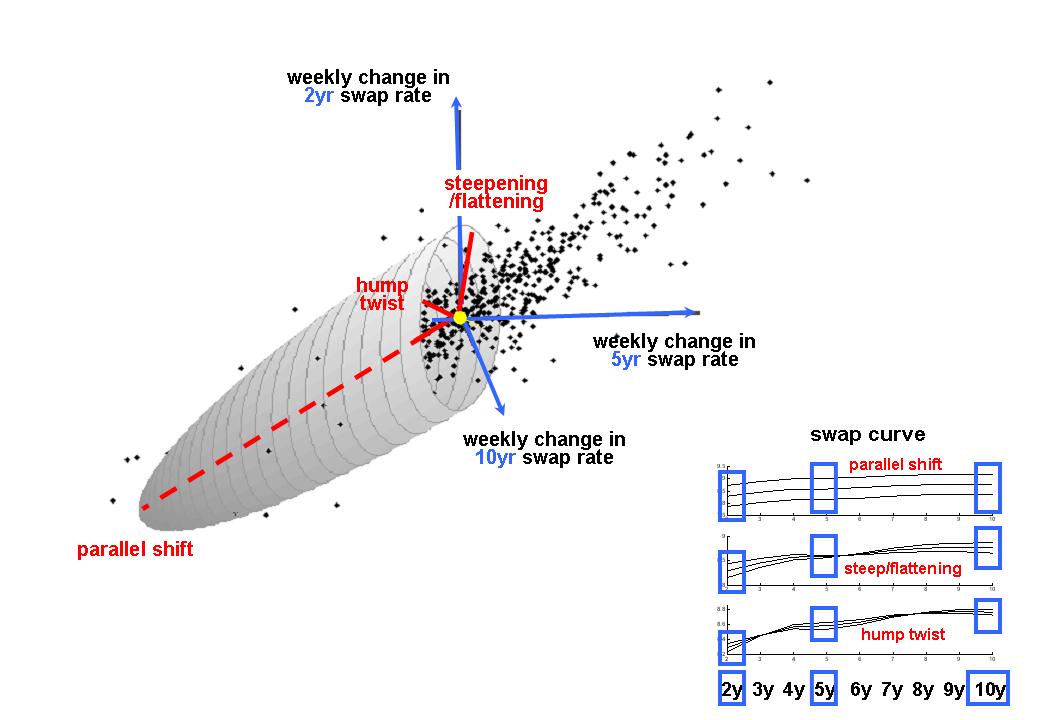

AMeucciRiskandAssetAllocationRoutines/Ch3_ModellingMarket/E_CaseStudySwap/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/A_Introduction/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/B_NonParametric/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/C_MaximumLikelihood/A_UnivariateNormal/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/C_MaximumLikelihood/B_UnivariateLognormal/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/C_MaximumLikelihood/C_MultivariateNormal/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/C_MaximumLikelihood/D_MultivariateT/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/D_Shrinkage/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/E_Robust/A_Intro/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/E_Robust/B_HubertM/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/E_Robust/C_HighBreakDown/

AMeucciRiskandAssetAllocationRoutines/Ch4_EstimatingInvariants/F_MissingData/

AMeucciRiskandAssetAllocationRoutines/Ch5_EvaluatingAllocations/A_StochasticDominance/

AMeucciRiskandAssetAllocationRoutines/Ch5_EvaluatingAllocations/B_ExpectedUtility/

AMeucciRiskandAssetAllocationRoutines/Ch5_EvaluatingAllocations/C_ValueAtRisk/

AMeucciRiskandAssetAllocationRoutines/Ch5_EvaluatingAllocations/D_ExpectedShortfall/

AMeucciRiskandAssetAllocationRoutines/Ch6_OptimizingAllocations/A_AnalyticalExample/

AMeucciRiskandAssetAllocationRoutines/Ch6_OptimizingAllocations/B_MeanVarianceFramework/Analytitcal/

AMeucciRiskandAssetAllocationRoutines/Ch6_OptimizingAllocations/B_MeanVarianceFramework/Generic/

AMeucciRiskandAssetAllocationRoutines/Ch6_OptimizingAllocations/C_TotalReturnVsBenchmark/

AMeucciRiskandAssetAllocationRoutines/Ch6_OptimizingAllocations/D_CaseStudy/

AMeucciRiskandAssetAllocationRoutines/Ch7_BayesianEstimation/

AMeucciRiskandAssetAllocationRoutines/Ch8_EvalEstimationRisk/A_EvaluationGeneric/

AMeucciRiskandAssetAllocationRoutines/Ch8_EvalEstimationRisk/B_PriorAllocation/

AMeucciRiskandAssetAllocationRoutines/Ch8_EvalEstimationRisk/C_SampleBasedAllocation/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/A_BayesAllocation/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/B_BlackLittAllocation/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/C_RobustAllocation/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/C_RobustAllocation/SeDuMi_1_1/

AMeucciRiskandAssetAllocationRoutines/Ch9_OptimEstimationRisk/D_RobustBayesAllocation/

AMeucciRiskandAssetAllocationRoutines/Extras/COP/

AMeucciRiskandAssetAllocationRoutines/Extras/IntroMATLAB/

You can also select a web site from the following list

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)

Asia Pacific

- Australia (English)

- India (English)

- New Zealand (English)

- 中国

- 日本Japanese (日本語)

- 한국Korean (한국어)